Most people dream about retiring early.

Very few truly understand what it takes to make it work.

Because retiring at 55 isn’t just about having savings…

It’s about making those savings last for 30+ years without a paycheck.

Today, I’m going to walk you through a real-life case that shows exactly what’s at stake—and what it takes to get it right.

Meet David: A Retirement Plan on the Edge

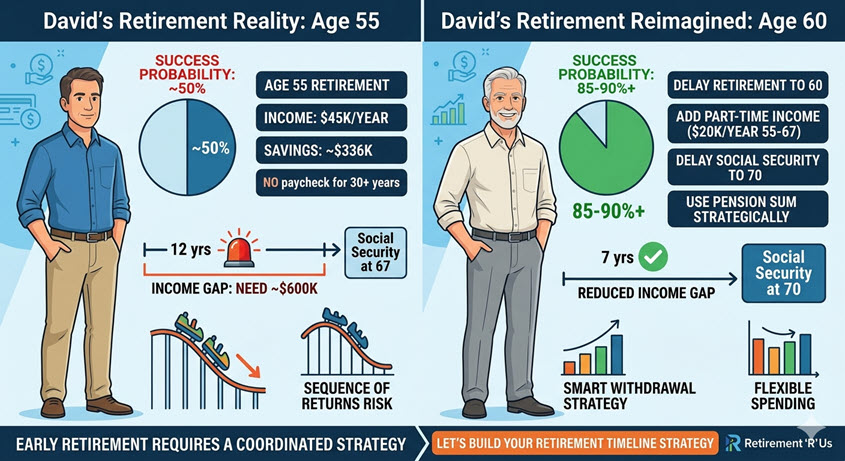

David is 53 years old, single, and works in HVAC in Tampa, Florida.

Here’s where he stands today:

- Income: $45,000/year

- Retirement goal: Age 55 (just 2 years away)

- Spending target: $50,000/year

- Total savings: ~$336,000

- Pension: $30,000 lump sum

- Social Security: ~$1,850/month at 67

- Housing: Renting

On the surface, it feels possible.

But when we ran 10,000 retirement simulations, the results told a different story:

❗ Success Probability: ~50%

That means this plan fails about half the time.

Why Early Retirement Is So Challenging

David’s biggest issue isn’t overspending.

It’s timing.

Retiring at 55 creates a massive gap:

- 12 years before Social Security

- No guaranteed lifetime pension income

- Heavy reliance on investments early

This introduces the biggest risk in retirement planning:

Sequence of returns risk

If the market drops early in retirement, it can permanently damage the plan—even if it recovers later.

The Retirement Timeline Strategy: Why Timing Matters More Than You Think

One of the biggest mistakes people make is thinking retirement is a single decision.

It’s not.

Retirement unfolds in phases—and each phase requires a different strategy.

Here’s how David’s retirement breaks down:

Pre-Retirement (Age 53–55) — Preparation Years

David is here right now.

- Final opportunity to increase savings

- Critical planning decisions

- Very little margin for error

👉 Focus:

Maximize preparation before retirement begins

Early Retirement (55–67) — The Risk Zone

This is the most fragile part of David’s plan.

- No Social Security yet

- No steady pension income

- Portfolio must fund everything

👉 Reality:

David needs roughly $600,000 to cover this period alone

($50,000 × 12 years)

👉 Focus:

Managing withdrawals and protecting against market risk

Middle Retirement (67–73) — Coordination Years

- Social Security begins

- Income becomes more stable

- Portfolio pressure decreases

👉 Focus:

Coordinating income sources and managing taxes

Late Retirement (73+) — Preservation Years

- Required Minimum Distributions (RMDs) begin

- Taxable income increases

- Flexibility declines

👉 Focus:

Protecting assets and maintaining income efficiency

The Core Problem: The Income Gap

The math is simple—but powerful:

- Needed from age 55–67: ~$600,000

- Available assets: ~$336,000

That gap is what drives the low success rate.

So… Can David Retire at 55?

Yes—but not without adjustments.

Let’s look at what actually moves the needle.

The Turning Point: Strategic Adjustments

1. Delay Retirement (Even Slightly)

Moving retirement from 55 to 58 or 60 changes everything:

- Fewer withdrawal years

- More time to save

- Higher Social Security benefits

Impact:

Success rate improves to 65–75%+

2. Add Part-Time Income (Massive Impact)

Even modest income dramatically improves outcomes.

Example:

- $20,000/year from age 55–67

Result:

- Reduces portfolio withdrawals significantly

- Extends portfolio life

This can increase success probability by 15–20%

3. Delay Social Security to Age 70

- Higher guaranteed income

- Less reliance on investments later

👉 Critical for long-term stability

4. Use the Pension Lump Sum Strategically

Instead of spending it early:

- Allocate it as a bridge fund

- Cover early retirement years

👉 Reduces stress on investment accounts

5. Implement a Smart Withdrawal Strategy

- Use taxable assets first

- Manage tax brackets carefully

- Preserve flexibility

👉 Helps avoid unnecessary tax drag

6. Stay Flexible With Spending

- Reduce spending during downturns

- Increase when markets are strong

👉 Flexibility alone can improve outcomes by 10%+

What Happens After Optimization?

After applying these strategies:

| Scenario | Success Rate |

|---|---|

| Retire at 55 (no changes) | ~50% |

| Retire at 58 + part-time income | ~75–85% |

| Retire at 60 + optimized strategy | 85–90%+ |

The Biggest Lesson From David’s Story

Early retirement isn’t about hitting a magic number.

It’s about managing:

- Time

- Risk

- Income gaps

David didn’t need:

- More complexity

- Riskier investments

He needed:

A realistic timeline and a coordinated strategy

What This Means for You

If you’re considering early retirement, ask yourself:

- How many years until Social Security begins?

- Where will your income come from during that gap?

- How exposed is your plan to early market downturns?

Because here’s the truth:

The earlier you retire, the more precise your strategy needs to be

Final Thought

Early retirement is possible.

But it’s not forgiving.

You don’t get:

- A redo on withdrawal mistakes

- A second chance at market timing

- Extra years to recover

That’s why planning matters.

The goal isn’t just to retire early…

it’s to stay retired

Ready to Build Your Retirement Plan?

At Retirement ‘R’ Us, we help people:

- Evaluate early retirement realistically

- Close income gaps

- Build sustainable income strategies

If you want to know:

- When you can retire

- How confident your plan really is

- What changes make the biggest impact

We’re here to help.

Next Step

Let’s build your personalized Retirement Timeline Strategy.

Important Disclosures: Retirement “R” Us, a registered retirement planning advisor, provides this information for educational purposes only. It is not intended to offer personalized investment advice or suggest that any discussed securities or services are suitable for any specific investor. Readers should not rely solely on the information provided here when making investment decisions.

- Investing carries risks, including the potential loss of principal. No investment strategy can ensure a profit or protect against loss during market downturns.

- Past performance is not indicative of future results.

- The opinions shared are not meant to serve as investment advice or to predict future performance.

- While we believe the information provided is reliable, we do not guarantee its accuracy or completeness.

- This content is for educational purposes only and is not intended as personalized advice or a guarantee of achieving specific results. Consult your tax and financial advisors before implementing any discussed strategies.

- Everyone’s retirement circumstances, especially when it comes to health insurance and health care, are unique.

- Retirement “R” Us does not provide tax or legal advice. Please consult your tax advisor or attorney for advice tailored to your situation.

Legal Disclaimer: The information provided on this website is for general informational purposes only and is not intended to be legal advice. While we strive to ensure the accuracy and completeness of the information, we make no guarantees regarding its accuracy, completeness, or timeliness. The content is provided “as is” without any warranties of any kind, either express or implied.

Use of this website does not create an attorney-client relationship between the user and the website owner or any of its contributors. Users should not act upon the information provided without seeking professional legal counsel. Any reliance on the information provided is solely at the user’s own risk.

We are not responsible for any errors or omissions, or for any actions taken based on the information provided on this website. Links to third-party websites are provided for convenience only and do not constitute an endorsement or approval of their content. We are not liable for any damages arising from the use of or reliance on the information provided on this website or any linked third-party websites.

By using this website, you agree to the terms of this legal disclaimer. If you do not agree with these terms, please do not use this website.

Leave a Reply