-

“The final chapter of retirement isn’t about accumulating wealth. It’s about protecting it, enjoying it, and passing it on with purpose.” Grant is now in his late seventies. The retirement they dreamed about years earlier has become their reality. They’ve explored the country in their RV, watched their son graduate from college, celebrated anniversaries, welcomed…

-

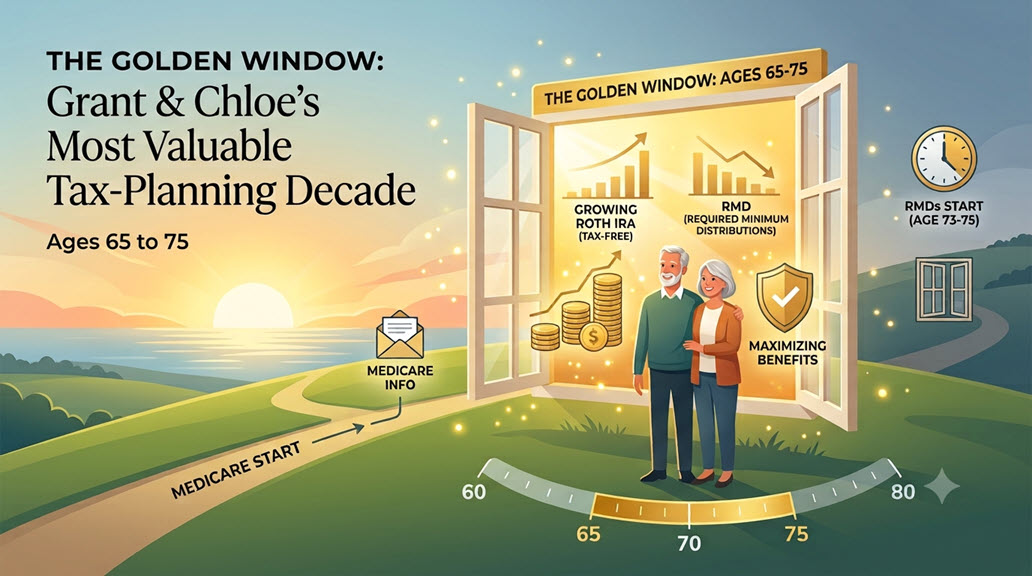

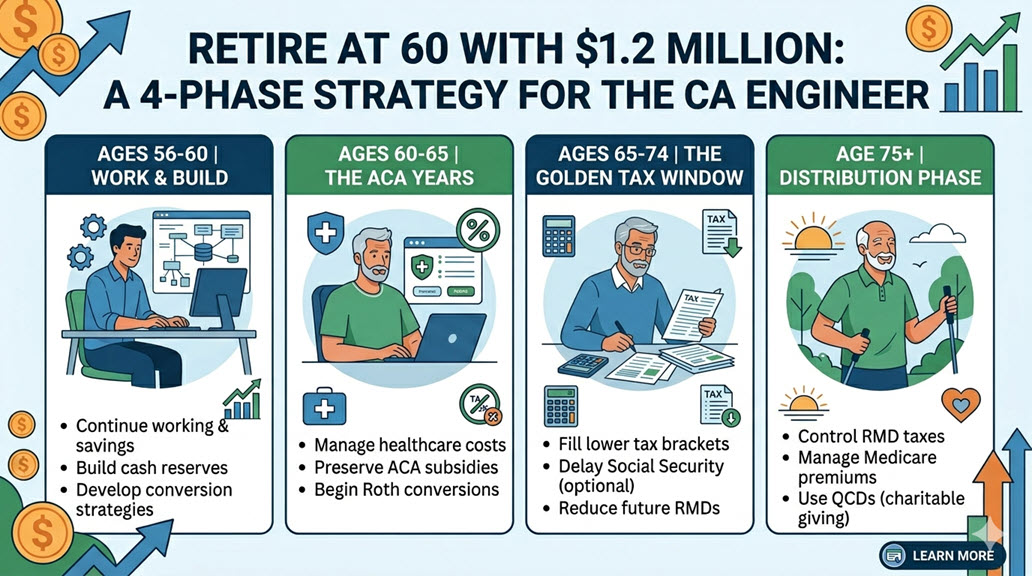

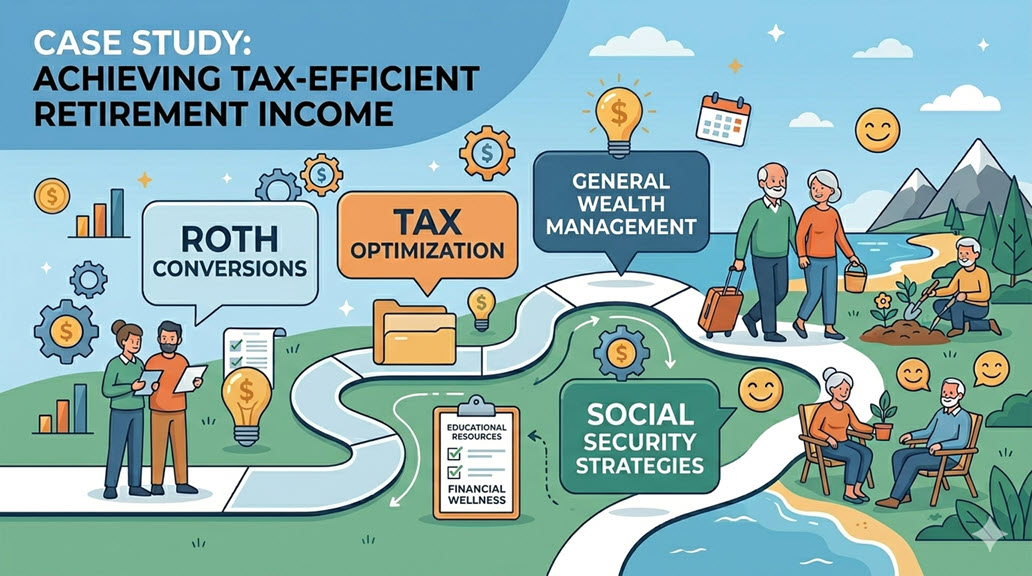

“The biggest retirement tax savings often come from taxes you choose to pay—not the ones you’re forced to pay.” Grant turns 65. A few weeks before his birthday, a familiar envelope arrives in the mail. It’s his Medicare enrollment information. For many Americans, turning 65 marks another retirement milestone. Healthcare coverage shifts from the Affordable…

-

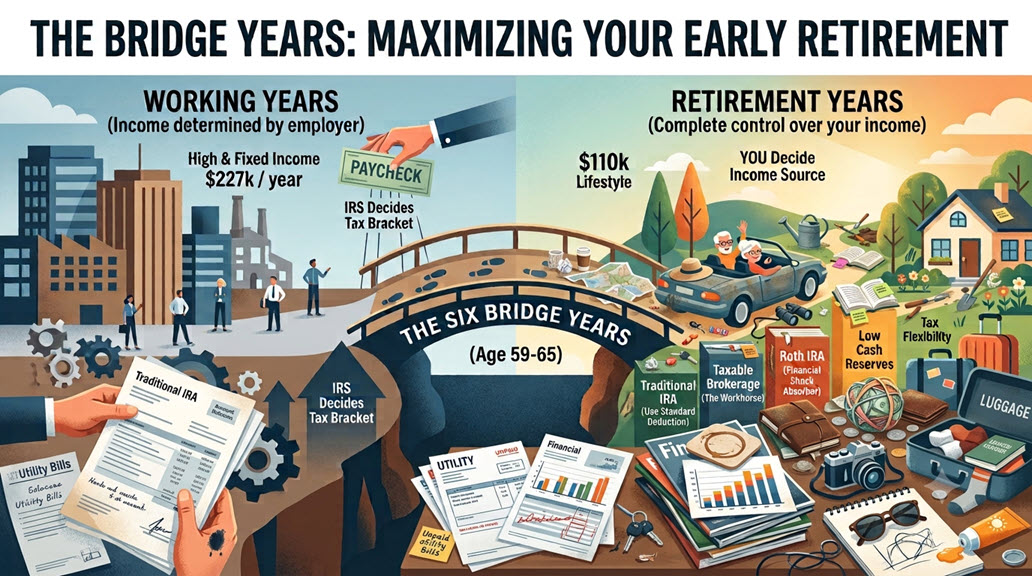

As Grant heads home after his final day on the job, one thought keeps replaying in his mind. “I finally don’t have to worry about earning a paycheck anymore.” And he’s right. But a new challenge has quietly taken its place. For the first time in nearly four decades, Grant and Chloe have complete control…

-

On a warm Friday afternoon, just a few months before his 60th birthday, Grant Lawson shuts down his computer for the last time. After nearly four decades of working as a Financial Manager and Controller, he’s ready for the next chapter. There are no more quarterly reports, no more budget meetings, and no more late-night…

-

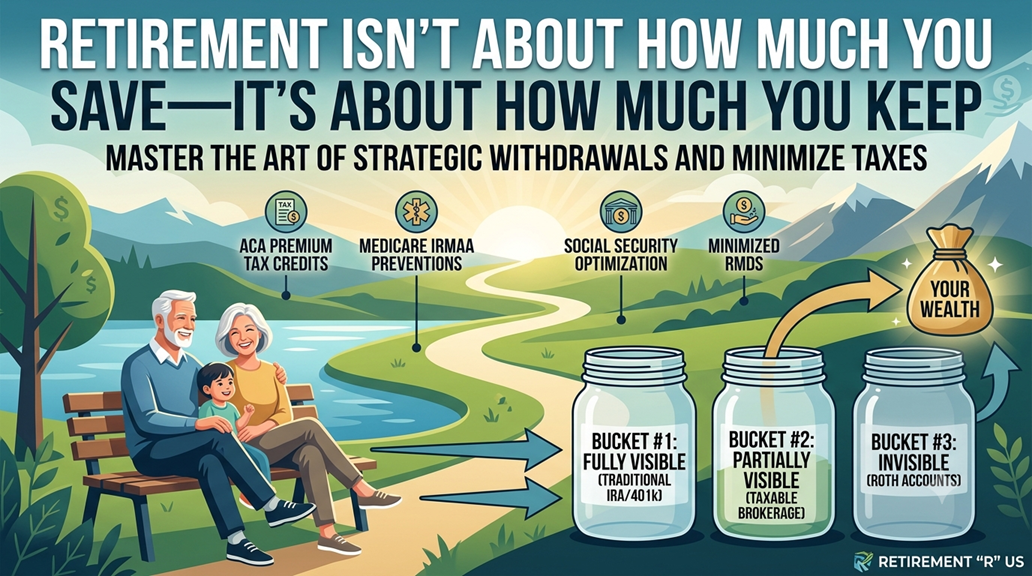

Most people assume retirement success depends on reaching some magic number like $2 million or $3 million. But retirement isn’t simply about accumulating wealth. It is about converting decades of savings into sustainable income while minimizing taxes, managing healthcare costs, and preserving flexibility for the next 30 years. Let’s look at the case of Bobby…

-

👩💼 Overview Snapshot At 50, with nearly $1 million in assets and a federal pension on the horizon, Karen has a powerful foundation. But the real work — and the real opportunity — lies in the decade ahead. Metric Value Description Investable Assets $906K Across all accounts Target Spending $65K Per year in retirement Retirement…

-

Who Is This Person? This case study follows a 52‑year‑old single man living in Stockton, California. He is not wealthy. He does not own a home. He does not have a pension, inheritance, or multiple retirement accounts. What he does have is one Roth IRA, a disciplined approach to money, and a lifestyle intentionally designed…

-

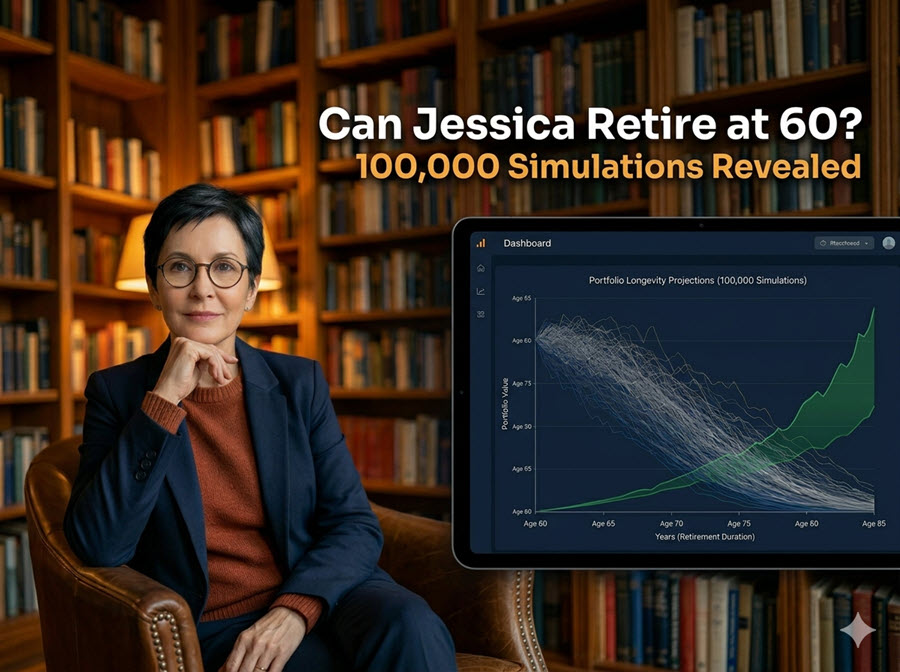

Retirement planning can feel like navigating a financial minefield — one wrong step, and your nest egg might not last as long as you need it to. Today, we analyze Jessica White’s retirement plan using Monte Carlo simulations, a powerful statistical method that tests 100,000 possible market scenarios to estimate the likelihood of her savings…

-

Meet Eric and Olivia Benson. At 63 and 60, they’re standing at the edge of a major life transition. Eric has spent his career in the nonprofit world; Olivia is a librarian. They live in Reno, Nevada, own their $360,000 home outright, and plan to retire when Eric turns 65 and Olivia turns 62—just two…

-

When Jessica White, a librarian in Baltimore, sat down to plan her retirement at 57, she thought she’d done everything right. She’d accumulated $505,000 across a 401(k), Traditional IRA, Roth IRA, HSA, and taxable brokerage. She was on track to retire at 60. By most measures, she was ahead of schedule. Then she ran the…