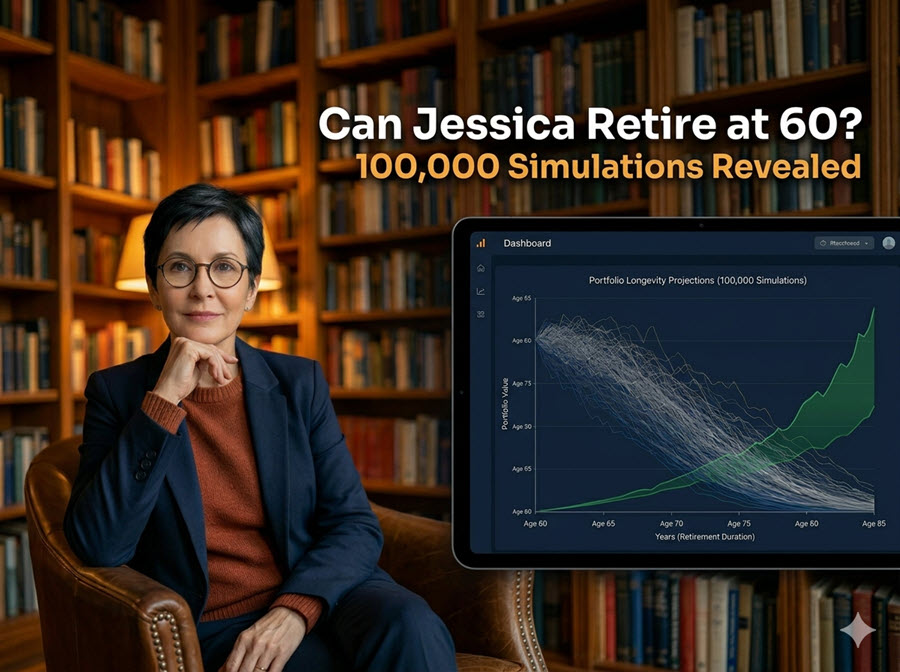

Retirement planning can feel like navigating a financial minefield — one wrong step, and your nest egg might not last as long as you need it to. Today, we analyze Jessica White’s retirement plan using Monte Carlo simulations, a powerful statistical method that tests 100,000 possible market scenarios to estimate the likelihood of her savings surviving through retirement.

Meet Jessica White: A Baltimore Librarian Planning to Retire at 60

Her Financial Snapshot

| Age | 57 |

| Household Type | Single |

| Occupation | Librarian, Baltimore MD |

| Target Retirement Age | 60 |

| Planning Horizon | Age 85 (25 years in retirement) |

| Annual Income (current) | $80,000 |

| Annual Spend in Retirement | $75,000 |

| Annual Healthcare Cost | $6,000 |

| 401(k) | $350,000 |

| Traditional IRA | $50,000 |

| Roth IRA | $75,000 |

| Taxable Brokerage | $250,000 |

| Cash / Money Market Funds | $22,500 |

| Total Portfolio (Today) | $747,500 |

| Pension (starting age 65) | $12,000/year |

| Social Security (starting age 67) | $2,100/month ($25,200/year) |

| Home Status | Renter (no home equity) |

The Big Question: Will Her Money Last to Age 85?

To answer this, we ran 100,000 Monte Carlo simulations. Each simulation randomly draws annual market returns and applies them to Jessica’s growing portfolio while factoring in inflation-adjusted spending and income. Here are the key parameters:

Note: The projected portfolio at retirement ($881,087) reflects three additional years of 5% investment growth plus $5,000/year in savings (the difference between Jessica’s $80,000 income and $75,000 spending) between now and age 60.

Key Findings

- ❌ Failure Rate: 86.7% — In nearly 87 out of 100 simulations, Jessica runs out of money before age 85.

- ✅ Success Rate: 13.3% — Only 1 in 7 simulated futures ends with a solvent portfolio at 85.

- ⚠️ Median Portfolio Depleted by Age 77 — Eight years before her planning horizon, in the median scenario the money is gone.

- 📉 Earliest Failure: Age 66 — In worst-case scenarios, the portfolio collapses just six years into retirement.

Why the 86.7% Failure Risk?

1. The Income Gap Before Age 65

From age 60 to 65, Jessica has zero guaranteed income. She must draw the full $81,000 per year (spending + healthcare) directly from her portfolio. Over five years, that’s roughly $405,000 in nominal withdrawals — nearly half her starting balance — before markets have had sufficient time to compound in her favor.

2. A 9.2% Withdrawal Rate in Year One

Financial planners traditionally cite the “4% Rule” as a safe withdrawal rate. Jessica’s baseline plan requires withdrawing approximately 9.2% of her portfolio annually in the first year ($81,000 ÷ $881,087) — more than double the safe threshold. This withdrawal rate almost guarantees portfolio depletion over a 25-year horizon.

3. Inflation Pressure is Severe at 3.3%

Today’s 3.3% CPI inflation rate is not benign for retirees. At this rate, the $81,000 in spending Jessica needs today becomes over $113,000 by the time she reaches 75. Her pension and Social Security, even if partially indexed, struggle to keep pace when retirement began at 60 with no income for five years.

4. No Home Equity Safety Net

As a renter, Jessica has no home equity to tap as a last resort. Homeowners can downsize, relocate, or access a reverse mortgage. Jessica does not have this option, making it even more critical that her portfolio stays intact throughout retirement.

How Can Jessica Improve Her Odds?

Scenario Results at a Glance

| Strategy | Success Rate | vs. Baseline |

|---|---|---|

| Baseline — Retire at 60, spend $75K/yr, SS at 67 | — | |

| Delay SS to Age 70 (32% larger benefit) | +2.0 pts | |

| Retire at Age 62 Instead of 60 | +13.0 pts | |

| Part-Time Income ($20K/yr) Until Age 67 | +16.2 pts | |

| Reduce Spending to $60,000/Year | +47.3 pts | |

| Combined: $65K spend + Part-Time + SS at 70 | +56.8 pts |

1. Reduce Annual Spending to $60,000–$65,000

Highest ImpactCutting retirement spending from $75,000 to $60,000 alone pushes the success rate from 13.3% to 60.6% — nearly a five-fold improvement. Review discretionary categories: travel, dining, subscriptions, and lifestyle inflation. A $65,000 target is more realistic while still dramatically improving outcomes. This single lever has more power than any other change Jessica can make.

2. Work Part-Time (Even $20,000/yr) Until Age 67

High ImpactA part-time librarian position, tutoring, consulting, or any income stream of $20,000 per year from ages 60–67 reduces portfolio withdrawals during the most critical early-retirement window. This alone lifts the success rate to 29.5%, and when combined with spending reductions, is transformative. Many libraries welcome experienced retirees in reduced-hour or part-time roles.

3. Maximize Savings in the Next 3 Years

Medium ImpactAt 57, Jessica is eligible for 401(k) catch-up contributions — an extra $7,500 per year above the standard limit in 2026. Aggressively maximizing pre-tax contributions over the next three years could add $30,000–$50,000 to her retirement balance. Every dollar saved now has three years to compound before withdrawals begin.

4. Delay Social Security to Age 70

Medium Impact. Every year Jessica delays claiming Social Security past 67 increases her benefit by approximately 8%. Waiting until 70 grows her monthly benefit from $2,100 to roughly $2,772/month ($33,264/year). While delaying alone adds only modest percentage points, combined with other strategies, the lifetime income boost is significant — especially across a 25-year horizon.

5. The Combined Strategy: Target 70%+ Success

Structural FixOur simulations show that combining a modest spending reduction ($65,000/year), part-time income until 67, and delaying Social Security to 70 pushes the success rate to 70.1%. This is still short of the 80–90% threshold most financial planners recommend, but it represents a fundamentally viable retirement versus a near-certain failure. Add two more working years — retiring at 62 instead of 60 — and the odds improve even further.

Final Verdict: Critical Action Required

Jessica White is a diligent saver who has done many things right. Her portfolio of nearly $750,000 at age 57 — built on a librarian’s salary — reflects genuine financial discipline. But the intersection of an ambitious early retirement age, a 25-year planning horizon, and today’s elevated 3.3% inflation rate creates a gap that her current plan simply cannot bridge.

The Monte Carlo results are not a sentence — they are a map. The simulations reveal precisely where the stress points are (the income gap from 60–67, the high early withdrawal rate, and inflation-related erosion) and exactly which levers are most powerful. With targeted adjustments, Jessica’s success rate can move from a perilous 13% to a defensible 70% or higher.

Retirement is not binary — fully retired at 60 or working forever at a desk. There is a middle path: a semi-retirement with part-time work she chooses, a slightly leaner budget in the early years, and Social Security timed for maximum lifetime impact. That path, according to 100,000 simulated futures, looks considerably brighter.

Would you make adjustments in Jessica’s position, or stick to the original plan? Let us know in the comments!

Want us to analyze a different retirement profile? Drop your scenario in the comments below, and we’ll run the numbers!

Important Disclosures: Retirement “R” Us, a registered retirement planning advisor, provides this information for educational purposes only. It is not intended to offer personalized investment advice or suggest that any discussed securities or services are suitable for any specific investor. Readers should not rely solely on the information provided here when making investment decisions.

- Investing carries risks, including the potential loss of principal. No investment strategy can ensure a profit or protect against loss during market downturns.

- Past performance is not indicative of future results.

- The opinions shared are not meant to serve as investment advice or to predict future performance.

- While we believe the information provided is reliable, we do not guarantee its accuracy or completeness.

- This content is for educational purposes only and is not intended as personalized advice or a guarantee of achieving specific results. Consult your tax and financial advisors before implementing any discussed strategies.

- Everyone’s retirement circumstances, especially when it comes to health insurance and health care, are unique.

- Retirement “R” Us does not provide tax or legal advice. Please consult your tax advisor or attorney for advice tailored to your situation.

Legal Disclaimer: The information provided on this website is for general informational purposes only and is not intended to be legal advice. While we strive to ensure the accuracy and completeness of the information, we make no guarantees regarding its accuracy, completeness, or timeliness. The content is provided “as is” without any warranties of any kind, either express or implied.

Use of this website does not create an attorney-client relationship between the user and the website owner or any of its contributors. Users should not act upon the information provided without seeking professional legal counsel. Any reliance on the information provided is solely at the user’s own risk.

We are not responsible for any errors or omissions, or for any actions taken based on the information provided on this website. Links to third-party websites are provided for convenience only and do not constitute an endorsement or approval of their content. We are not liable for any damages arising from the use of or reliance on the information provided on this website or any linked third-party websites.

By using this website, you agree to the terms of this legal disclaimer. If you do not agree with these terms, please do not use this website.

Leave a Reply