Roth IRAs offer tax-free growth and tax-free withdrawals in retirement—but only if you follow the rules. One of the most misunderstood aspects is the “5-year rule”, which plays a different role depending on your age and what kind of withdrawal you’re making (contributions, earnings, or conversions).

Let’s break down how the 5-year rule works before age 59½, at 59½, and after age 59½, with clear examples and a table for comparison.

Quick Primer: What Is the Roth IRA 5-Year Rule?

There are actually three separate 5-year rules in Roth IRA planning:

- For contributions, it governs when earnings can be withdrawn tax-free.

- For conversions, it governs when you can withdraw converted amounts penalty-free.

- For beneficiaries – applies to inherited Roth IRAs.

This post focuses on the first two as they relate to your own Roth IRA.

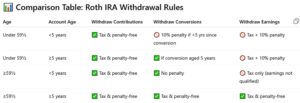

1. Under Age 59½

If you’re under 59½, withdrawals from your Roth IRA fall under stricter rules. Here’s how it works:

- Contributions: Can always be withdrawn tax and penalty-free, no matter your age or how long the money has been in the account.

- Earnings: Taxable and subject to a 10% early withdrawal penalty, unless it’s a qualified distribution (i.e., meets the 5-year rule and you’re 59½ or older).

- Conversions: Withdrawals of converted amounts within 5 years may trigger a 10% penalty, even if you’ve paid taxes on the conversion.

Example 1: Jill, age 45

- Started Roth IRA in 2010.

- Contributed $50,000 over the years and has $20,000 in earnings.

- Wants to withdraw $30,000.

✅ She can withdraw $30,000 from contributions tax and penalty-free.

If she goes beyond that and touches the $20,000 in earnings, she pays tax + 10% penalty.

Example 2: Alex, age 50

- Converted $40,000 from a traditional IRA to Roth in 2023.

- Wants to withdraw $10,000 in 2025.

That $10,000 withdrawal is subject to a 10% penalty because the conversion hasn’t aged 5 years yet (i.e., until 2028).

2. At Age 59½ (But Roth IRA is <5 Years Old)

Turning 59½ eliminates the 10% penalty, but not the tax. If your first Roth IRA contribution is less than 5 years old, you still owe income tax on the earnings.

Example 3: Maria turns 59½ in 2025

- Opened her first Roth IRA in 2022.

- Withdraws $15,000 (includes $5,000 in earnings) in 2025.

✅ No 10% penalty due to her age.

But she pays income tax on the $5,000 in earnings because her account is only 3 years old.

3. Over Age 59½ and Roth Open ≥5 Years

This is the sweet spot of Roth IRA withdrawals: If you’re over 59½ and your Roth IRA has been open at least 5 years, all withdrawals—contributions and earnings—are tax- and penalty-free.

Example 4: Tom, age 62

- Opened Roth IRA in 2017.

- Has $100,000 in the account: $70,000 contributions, $30,000 earnings.

- Wants to withdraw $40,000.

✅ The entire $40,000 is tax-free and penalty-free.

✅ Key Takeaways

- Contributions can always be withdrawn tax- and penalty-free.

- The 5-year clock starts Jan 1 of the year you first contribute to any Roth IRA.

- Conversions have their own 5-year clock (one per conversion).

- Once you’re over 59½ and the Roth is 5+ years old, you’ve unlocked the full tax-free benefit.

Final Tip: Track Your Roth Sources Carefully

It’s crucial to keep records of:

- Your original contribution year

- Each Roth conversion and the year it was made

- Your current age

This info ensures you don’t accidentally trigger taxes or penalties on early withdrawals.

Important Disclosures: Retirement “R” Us, a registered retirement planning advisor, provides this information for educational purposes only. It is not intended to offer personalized investment advice or suggest that any discussed securities or services are suitable for any specific investor. Readers should not rely solely on the information provided here when making investment decisions.

- Investing carries risks, including the potential loss of principal. No investment strategy can ensure a profit or protect against loss during market downturns.

- Past performance is not indicative of future results.

- The opinions shared are not meant to serve as investment advice or to predict future performance.

- While we believe the information provided is reliable, we do not guarantee its accuracy or completeness.

- This content is for educational purposes only and is not intended as personalized advice or a guarantee of achieving specific results. Consult your tax and financial advisors before implementing any discussed strategies.

- Everyone’s retirement circumstances, especially when it comes to health insurance and health care, are unique.

- Retirement “R” Us does not provide tax or legal advice. Please consult your tax advisor or attorney for advice tailored to your situation.

Legal Disclaimer: The information provided on this website is for general informational purposes only and is not intended to be legal advice. While we strive to ensure the accuracy and completeness of the information, we make no guarantees regarding its accuracy, completeness, or timeliness. The content is provided “as is” without any warranties of any kind, either express or implied.

Use of this website does not create an attorney-client relationship between the user and the website owner or any of its contributors. Users should not act upon the information provided without seeking professional legal counsel. Any reliance on the information provided is solely at the user’s own risk.

We are not responsible for any errors or omissions, or for any actions taken based on the information provided on this website. Links to third-party websites are provided for convenience only and do not constitute an endorsement or approval of their content. We are not liable for any damages arising from the use of or reliance on the information provided on this website or any linked third-party websites.

By using this website, you agree to the terms of this legal disclaimer. If you do not agree with these terms, please do not use this website.

Leave a Reply