Early retirees tend to have one thing in common: they got there by taking risk. High stock allocations, aggressive growth strategies, maybe a heavy tilt toward technology or large-cap growth. It worked. They accumulated enough to retire decades ahead of schedule.

And then they make a critical mistake: they keep the same portfolio.

Why the Strategy That Got You Here Doesn’t Work There

Retirement investing and accumulation investing are fundamentally different problems. During accumulation, you’re adding money regularly. A market downturn is partly mitigated by continued contributions buying shares at lower prices. Sequence-of-returns risk is real, but it’s partially offset by your paychecks.

In retirement, you’re withdrawing. A downturn hits your principal directly, and if you’re drawing down while prices are depressed, you lock in losses and have fewer shares to benefit from the recovery. The same sequence of returns that was manageable during accumulation can be devastating during distribution.

This is why the data on safe withdrawal rates consistently shows that how you sequence your withdrawals matters as much as how much you withdraw. And it’s why the portfolio mix that got you here deserves a second look.

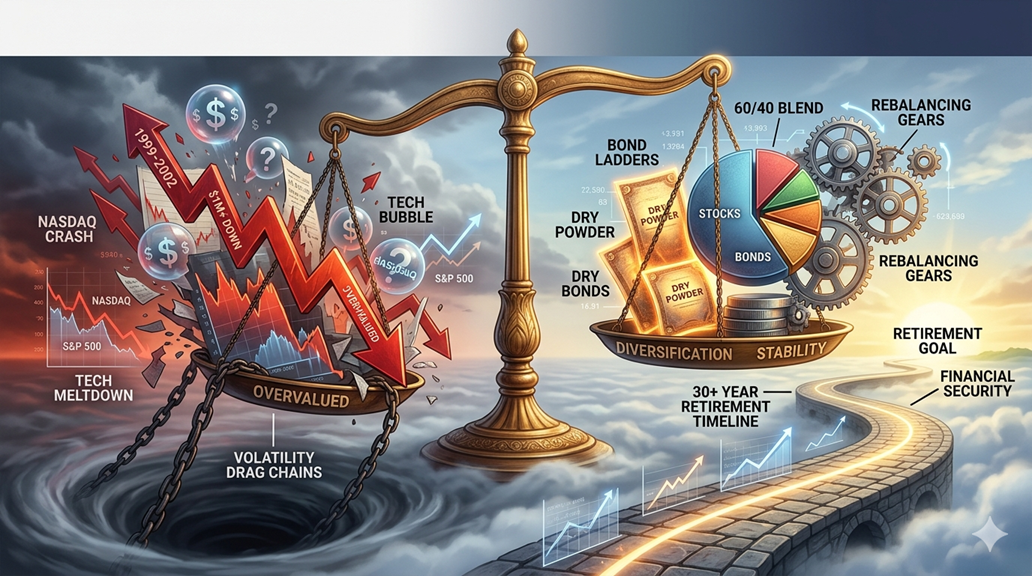

The Problem with 100% Stocks

For early retirees, one of the most common mistakes I see is maintaining a 90% or 100% stock portfolio into retirement. The argument is intuitive: stocks have historically returned more, you have a long time horizon, and bonds offer “paltry” yields.

The problem is that the data doesn’t actually support this approach for longevity.

Historical simulations run repeatedly show that a 100% stock portfolio often underperforms a balanced portfolio over 30+ year retirements. Not because stocks return less over long periods — they don’t — but because of volatility drag. When you have to sell stocks during downturns to cover living expenses, you sell low. That impermanence of losses can cascade.

More importantly: a severe early-retirement downturn (think 2000-2002 or 2008-2009) can permanently impair a heavily stock-weighted portfolio. Early retirees have more to lose from early bad years than traditional retirees, because they have more years ahead for those losses to compound.

What the Historical Data Actually Shows

Let’s run a quick mental simulation. A retiree in 1972 with $1 million invested in a diversified all-stock portfolio, withdrawing 4% annually — the simulation showed their money lasting roughly 30 years. Not bad.

Now change that to a 60/40 stock/bond portfolio — still withdrawing 4% — and the outcomes improve dramatically. The bonds provided the stability needed to avoid selling stocks at depressed prices during the worst years.

Start the same simulation in 1999 — peak of the tech bubble — and the contrast is even starker. The all-stock investor ran into serious trouble. A 60/40 portfolio sailed through.

The common thread: bonds (or other defensive assets) don’t have to outperform stocks to add value. They just have to not fall as much when stocks fall — and provide dry powder to rebalance into at market lows.

The Sub-Asset Class Trap

Here’s a subtler problem I see constantly: early retirees who are over-concentrated in large-cap growth stocks — often because that’s what drove their accumulation.

Large-cap growth — particularly tech-heavy indices — has had a remarkable run since 2009. If you arrived at early retirement in the last 15 years, a significant portion of your wealth may be sitting in these names. They were the engine of your growth.

But concentrated large-cap growth risk is real, and the historical data is sobering:

Starting in 1972, a broadly diversified all-stock portfolio (large, small, value, growth) lasted through a 30-year retirement more or less intact. A portfolio concentrated in large-cap growth? In some simulations, it barely lasted 20 years.

Starting in 1999 — the tech bubble peak — the story is similar. A diversified portfolio survived. A NASDAQ-heavy portfolio ran out of money in roughly a decade.

The point isn’t that tech stocks are bad. It’s that concentration within your stock sleeve, especially in one sub-asset class that has performed exceptionally well, carries risk that doesn’t show up until the cycle turns.

The Case for Genuine Diversification

Within your stock allocation, diversification across:

- Large cap and small cap

- Value and growth

- Domestic and international

- REITs and commodities (sometimes)

…provides something bonds alone can’t: participation in equity upside with meaningfully reduced concentration risk.

The best portfolio for early retirees doesn’t look exciting. It looks boring — a genuine blend of asset classes that don’t all move together.

Rebalancing: The Bonus You’re Giving Away

Here’s a point that gets overlooked: rebalancing isn’t just risk management. In a balanced portfolio, it’s an active return enhancer. When stocks fall and you rebalance by buying more bonds, you’re systematically buying low and selling high. Over time, that discipline adds return relative to a static portfolio.

Most early retirees who arrived through aggressive accumulation didn’t rebalance — they just held on. In retirement, the rebalancing bonus becomes more valuable, not less.

The Real Rule

If there’s one takeaway from all the historical data, it’s this: the portfolio that maximizes your probability of success as an early retiree is almost never 100% stocks — and often has more bonds than most people expect.

This doesn’t mean going conservative. A 60/40 portfolio still has significant growth exposure. It means acknowledging that the first decade of retirement is the most dangerous — and building a portfolio that can weather it without forcing you to sell depressed assets to cover living expenses.

The Bottom Line

Your accumulation strategy and your retirement strategy are different tools for different jobs. If you’re carrying the same portfolio you had at 40 into your early 50s of retirement, you’re taking undiversified risk that isn’t being rewarded the way it was.

Review your allocation. Stress-test it against early-retirement scenarios — particularly bad starts like 2000 or 2008. Make sure your bond sleeve is meaningful enough to provide genuine ballast, not just token exposure.

And if you’re heavily concentrated in any single sub-asset class — tech, large-cap growth, or anything else — start thinking about whether that concentration is intentional or accidental.

The goal isn’t to reduce returns. It’s to make sure the returns you have are actually yours to keep.

Important Disclosures: Retirement “R” Us, a registered retirement planning advisor, provides this information for educational purposes only. It is not intended to offer personalized investment advice or suggest that any discussed securities or services are suitable for any specific investor. Readers should not rely solely on the information provided here when making investment decisions.

- Investing carries risks, including the potential loss of principal. No investment strategy can ensure a profit or protect against loss during market downturns.

- Past performance is not indicative of future results.

- The opinions shared are not meant to serve as investment advice or to predict future performance.

- While we believe the information provided is reliable, we do not guarantee its accuracy or completeness.

- This content is for educational purposes only and is not intended as personalized advice or a guarantee of achieving specific results. Consult your tax and financial advisors before implementing any discussed strategies.

- Everyone’s retirement circumstances, especially when it comes to health insurance and health care, are unique.

- Retirement “R” Us does not provide tax or legal advice. Please consult your tax advisor or attorney for advice tailored to your situation.

Legal Disclaimer: The information provided on this website is for general informational purposes only and is not intended to be legal advice. While we strive to ensure the accuracy and completeness of the information, we make no guarantees regarding its accuracy, completeness, or timeliness. The content is provided “as is” without any warranties of any kind, either express or implied.

Use of this website does not create an attorney-client relationship between the user and the website owner or any of its contributors. Users should not act upon the information provided without seeking professional legal counsel. Any reliance on the information provided is solely at the user’s own risk.

We are not responsible for any errors or omissions, or for any actions taken based on the information provided on this website. Links to third-party websites are provided for convenience only and do not constitute an endorsement or approval of their content. We are not liable for any damages arising from the use of or reliance on the information provided on this website or any linked third-party websites.

By using this website, you agree to the terms of this legal disclaimer. If you do not agree with these terms, please do not use this website.

Leave a Reply