✨ Introduction: A Retirement That Breaks the Rules

Most retirement plans are built around a simple assumption:

The kids are grown… the house is quiet… and expenses begin to fall.

But for Charles and Sarah Dalton, retirement looks very different.

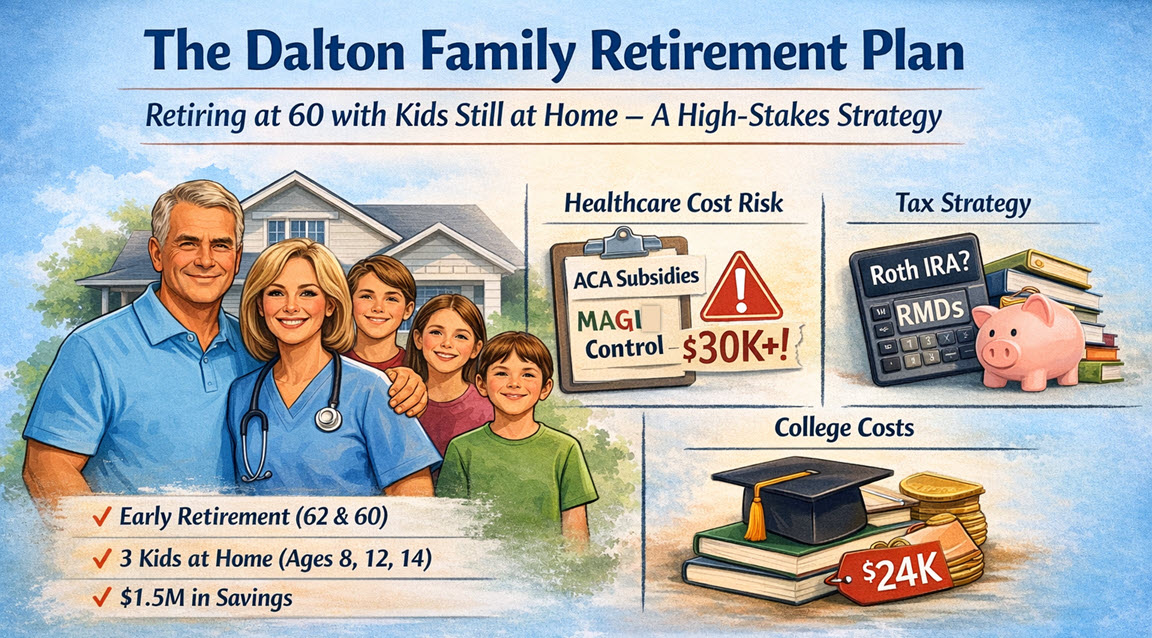

At ages 62 and 60, they’re ready to step away from full-time work — yet they still have three children at home (ages 8, 12, and 14).

This isn’t just retirement planning.

This is financial choreography under pressure.

And if done correctly, it works beautifully.

If done wrong, it falls apart quickly.

👨👩👧👦 Meet the Dalton Family

Charles spent decades in sales. Sarah built a steady career as a nurse. Together, they’ve done what many families strive for:

- Paid down their home

- Raised a family

- Built nearly $1.5 million in retirement savings

But their situation comes with unique complexity:

- They want to retire before Medicare (age 65)

- Their spending goal is $100,000/year

- Most of their wealth sits in pre-tax accounts

- And their children will depend on them financially for years to come

⚠️ The Hidden Problem Most Retirees Never See

On paper, the Daltons look ready.

But beneath the surface lies a critical issue:

👉 Their retirement success depends on ONE number

MAGI — Modified Adjusted Gross Income

This number will determine:

- How much they pay in taxes

- How much they pay for healthcare

- And whether retirement is comfortable… or stressful

🏥 The Healthcare Trap (Ages 60–65)

Here’s the reality most retirees underestimate:

Health insurance before age 65 can cost:

- $6,000/year… or

- $30,000+ per year

Same couple. Same coverage.

What determines the difference?

👉 Their income — specifically, their MAGI

💡 The Critical Threshold

For a married couple, once income crosses roughly:

$84,600

They lose access to key healthcare subsidies.

And the result is brutal:

A $1 increase in income

→ can trigger a $20,000+ increase in annual healthcare costs

🧠 The Strategy That Changes Everything

The Daltons don’t need less money.

They need better income design.

🎯 The Goal

- Spend: $100,000/year

- Show income: ~$60,000–$75,000

That gap is where the magic happens.

🔄 The “Structured Withdrawal Strategy”

Instead of pulling all their income from taxable sources, they carefully organize:

- Pension income

- Small IRA withdrawals

- Partial capital gains

- Brokerage principal (not taxable)

- Cash reserves

- Roth IRA withdrawals

Result:

- They meet their spending needs

- While keeping taxable income low

- And preserving healthcare subsidies

📌 Why This Works

Because:

Spending and taxable income are NOT the same thing

And retirees who understand this gain a massive advantage.

💰 The Tax Strategy Most People Get Wrong

Traditional advice says:

“Do Roth conversions early and often.”

But for the Daltons…

That advice could cost them tens of thousands per year.

🚫 What They Should NOT Do (Yet)

During ages 60–65:

- Large Roth conversions

- Excess IRA withdrawals

- Triggering unnecessary income

Why?

Because each dollar increases MAGI…

And risks blowing up their healthcare costs.

✅ What They SHOULD Do Instead

Ages 60–65:

- Keep income low

- Maximize healthcare subsidies

- Use taxable + Roth strategically

Ages 65–73:

- Begin targeted Roth conversions

- Take advantage of lower tax brackets

Age 73+:

- Manage Required Minimum Distributions (RMDs)

📈 Social Security: Timing is Everything

Charles and Sarah are eligible for Social Security at 67.

But claiming early would create two problems:

- Increase taxable income (hurting healthcare subsidies)

- Reduce their long-term guaranteed income

🎯 Recommended Strategy:

👉 Delay Social Security to at least age 67 (or even 70)

This allows them to:

- Keep income lower during critical years

- Maximize future benefits

- Reduce long-term portfolio pressure

🏡 The Home Decision

They currently own a home with:

- ~$198,000 in equity

For now, the best move is simple:

👉 Stay put

But later in retirement, this home becomes a powerful lever:

- Downsizing could unlock additional cash flow

- Reduce expenses

- Improve long-term sustainability

🎓 The Curveball: College Costs

With three kids still at home, college planning becomes unavoidable.

Current savings:

- $24,000 total

Which means…

👉 They are underfunded.

🎯 Smart Approach:

- Prioritize retirement first

- Use income control strategies to improve financial aid eligibility

- Supplement with cash flow and scholarships

⚖️ The Real Risk in This Plan

This plan works — but only with discipline.

The biggest threats:

- ❌ Poor income control (blowing past subsidy limits)

- ❌ Overspending early in retirement

- ❌ Ignoring tax strategy until it’s too late

- ❌ Market downturn early in retirement (sequence risk)

🟢 The Strengths That Make This Work

- Strong savings base (~$1.5M)

- Pension income for stability

- Taxable assets for flexibility

- A clear, structured withdrawal strategy

🧭 The Retirement Roadmap

Phase 1: Ages 60–65 (The Danger Zone)

- Control income aggressively

- Optimize healthcare subsidies

- Use structured withdrawals

Phase 2: Ages 65–73 (The Opportunity Window)

- Begin Roth conversions

- Manage tax brackets intentionally

Phase 3: Age 67–70

- Activate Social Security strategically

Phase 4: Age 73+

- Manage RMDs

- Reduce tax burden long-term

🏁 Final Verdict

Can Charles and Sarah retire today?

👉 Yes — but only if they follow the plan.

This is not a “set it and forget it” retirement.

It’s a precision strategy.

💡 Final Thought

The Dalton family teaches one of the most important lessons in modern retirement planning:

It’s no longer about how much you’ve saved…

It’s about how intelligently you use it.

A single misstep — even $1 too much in income — could cost them $20,000+ per year.

But with the right strategy?

They unlock:

- Lower taxes

- Affordable healthcare

- And a confident retirement — even with kids still at home

📣 Retirement ‘R’ Us Insight

This is the new era of retirement planning.

Where strategy beats savings.

And those who understand the rules…

get to retire on their terms.

Want a personalized version of this plan for your family? That’s exactly what we do at Retirement ‘R’ Us.

Important Disclosures: Retirement “R” Us, a registered retirement planning advisor, provides this information for educational purposes only. It is not intended to offer personalized investment advice or suggest that any discussed securities or services are suitable for any specific investor. Readers should not rely solely on the information provided here when making investment decisions.

- Investing carries risks, including the potential loss of principal. No investment strategy can ensure a profit or protect against loss during market downturns.

- Past performance is not indicative of future results.

- The opinions shared are not meant to serve as investment advice or to predict future performance.

- While we believe the information provided is reliable, we do not guarantee its accuracy or completeness.

- This content is for educational purposes only and is not intended as personalized advice or a guarantee of achieving specific results. Consult your tax and financial advisors before implementing any discussed strategies.

- Everyone’s retirement circumstances, especially when it comes to health insurance and health care, are unique.

- Retirement “R” Us does not provide tax or legal advice. Please consult your tax advisor or attorney for advice tailored to your situation.

Legal Disclaimer: The information provided on this website is for general informational purposes only and is not intended to be legal advice. While we strive to ensure the accuracy and completeness of the information, we make no guarantees regarding its accuracy, completeness, or timeliness. The content is provided “as is” without any warranties of any kind, either express or implied.

Use of this website does not create an attorney-client relationship between the user and the website owner or any of its contributors. Users should not act upon the information provided without seeking professional legal counsel. Any reliance on the information provided is solely at the user’s own risk.

We are not responsible for any errors or omissions, or for any actions taken based on the information provided on this website. Links to third-party websites are provided for convenience only and do not constitute an endorsement or approval of their content. We are not liable for any damages arising from the use of or reliance on the information provided on this website or any linked third-party websites.

By using this website, you agree to the terms of this legal disclaimer. If you do not agree with these terms, please do not use this website.

Leave a Reply